Tien Wong, Founder and Executive Chairman, CONNECTpreneur | March 3, 2026

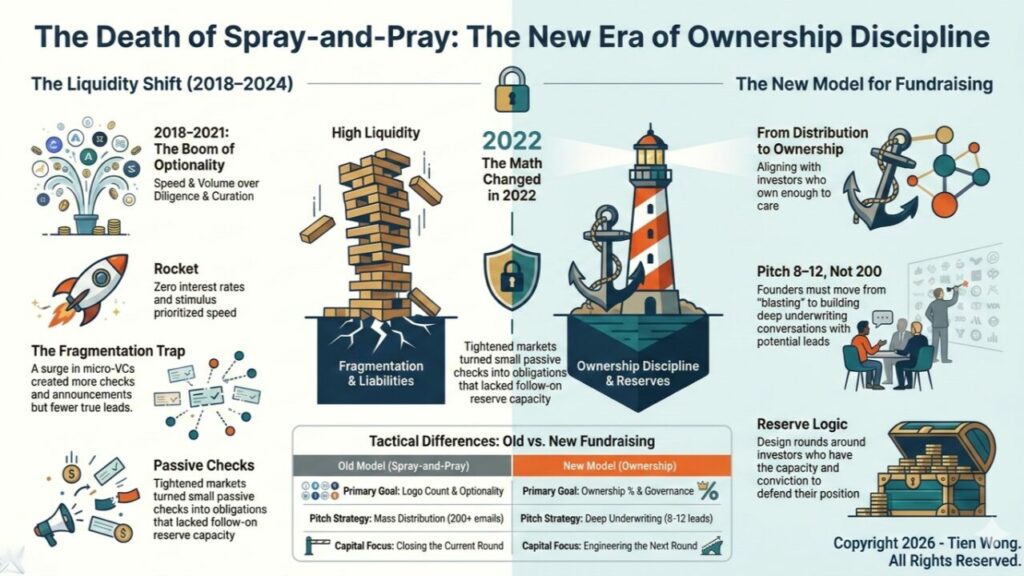

Spray-and-Pray fundraising didn’t die because capital disappeared.

It died because ownership, real ownership, started to matter again.

For a few years, volume worked.

Founders emailed hundreds of investors. Syndicates deployed at speed. Micro-VCs wrote small checks across dozens of companies. Rounds closed on momentum.

It wasn’t irrational.

It was liquidity.

But liquidity is not permanent.

And when liquidity changes, behavior must change.

A short timeline to set the stage:

2018–2019 Micro-VC proliferation accelerated. Angel syndicates scaled. Emerging managers launched sub-$50M funds. Capital access widened dramatically.

2020–2021 Zero interest rates. Stimulus liquidity. Record venture deployment. IPO window wide open. SPAC boom. Valuations expanded rapidly.

Speed beat diligence. Optionality beat concentration. Distribution beat curation.

In that environment, spray-and-pray wasn’t sloppy.

It was adaptive.

Late 2021 into 2022, public markets corrected sharply.

Growth multiples compressed. Biotech and other indices retrenched. The IPO window shut.

Private markets followed accordingly.

From 2022–2024, the system experienced:

Funds that deployed aggressively in 2020–2021 had to defend positions.

And here’s the structural truth:

Optionality investing only works when follow-on capital is abundant.

When liquidity tightens, every small passive check becomes a potential future obligation.

Ownership concentration and reserve capacity begin to matter more than logo count.

Spray-and-pray didn’t collapse because investors got pessimistic.

It collapsed because math changed.

Between 2018 and 2022:

More checks. More investors. More announcements.

But fewer true leads.

When markets tightened, many micro-funds lacked:

The system became over-fragmented.

The market didn’t lose capital.

It lost coordination.

From 2020–2022, LPs allocated heavily into:

This expansion wasn’t flawed.

But many funds were born at peak valuations.

When exits slowed and distributions dropped, new allocations tightened.

Emerging managers faced:

Which meant portfolio companies felt the pressure.

This wasn’t ideological.

It was cyclical.

Capital raised at the top of a liquidity cycle faces the hardest reset.

In 2021, strong companies:

It felt like success.

But when the market reset:

Easy capital created structural fragility.

Old model:

Blast. Hope. Stack logos. Assume follow-on.

New model:

Curate. Align. Concentrate. Own.

Investors now ask:

This isn’t contraction.

It’s professionalization.

This reset is not a drought.

It is a filter.

Weak underwriting is being removed. Loose governance is being punished. Uncommitted capital is retreating.

What remains is stronger.

When ownership concentrates, incentives align. When incentives align, governance improves. When governance improves, outcomes compound.

The next great companies will not be those that mastered distribution in 2021.

They will be those that engineered durable ownership in 2026.

The next top-decile funds will not be those that wrote the most checks.

They will be those that owned enough to matter — and had the reserves and conviction to defend it.

Spray-and-Pray was a liquidity behavior.

Ownership is a capital discipline.

And capital discipline is what creates long-term power.

The future belongs to those who build capital structures, not just capital rounds.

© Big Idea CONNECTpreneur. All rights reserved. 2024