Tien Wong, Founder and Executive Chairman, CONNECTpreneur | June 2, 2026

One of the most common statements I hear from life sciences CEOs is:

“We’re looking for strategic investors.”

Biotech founders say it.

Medtech founders say it.

Diagnostics founders say it.

Digital health founders say it.

Over the past two decades, my team and I have organized nearly 500 investor events, reviewed hundreds of life sciences companies, and spent countless hours with founders, investors, family offices, venture capital firms, corporate development teams, and strategic partners.

Along the way, I’ve noticed a pattern.

Many founders spend enormous amounts of time pursuing strategic investors.

Very few spend enough time understanding them.

The problem isn’t that strategic investors are bad.

The problem is that most founders fundamentally misunderstand why strategic investors invest in the first place.

That misunderstanding can cost companies months of time, precious runway, and in some cases, the opportunity to complete a financing altogether.

The story usually sounds something like this:

“We have a differentiated technology.”

“A large pharmaceutical company, medtech company, diagnostics company, or healthcare organization will recognize its value.”

“They will invest.”

“Their participation will validate the company.”

“Other investors will follow.”

The logic seems sound.

After all, a strategic investor understands the science.

They understand the market.

They understand the regulatory environment.

They may become a customer, commercial partner, licensing partner, distributor, or acquirer.

What founder wouldn’t want that?

The problem is that this entire narrative assumes the strategic investor wants what the founder wants.

In reality, they usually don’t.

This is the first misconception.

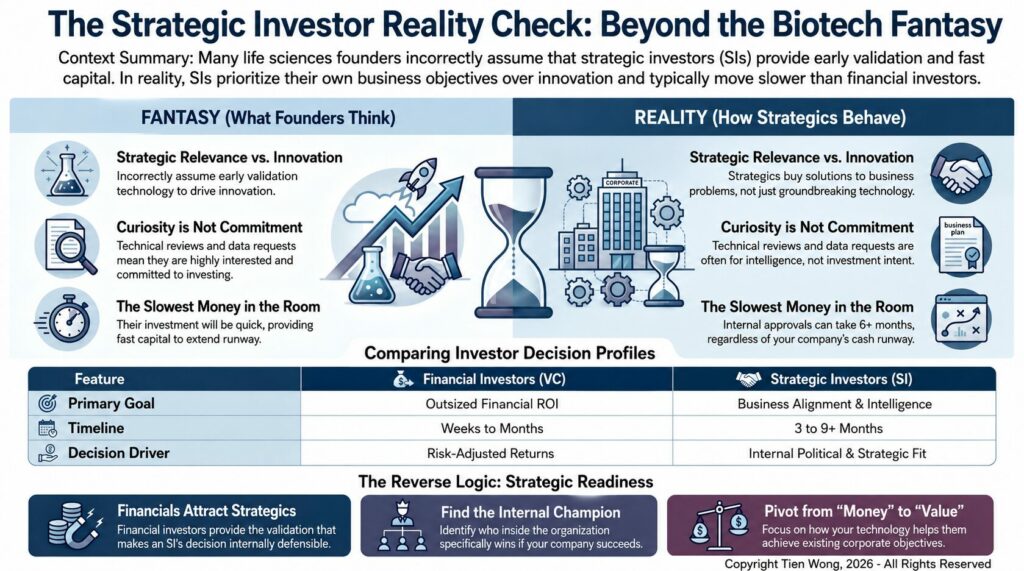

Founders often believe strategic investors are searching for the most innovative technologies.

That is rarely true.

Most strategic investors are not buyers of innovation.

They are buyers of strategic relevance.

That distinction matters.

A founder looks at a technology and asks:

“How groundbreaking is this?”

A strategic investor asks:

“How does this help us achieve an existing business objective?”

Those are very different questions.

A strategic investor may be evaluating whether your technology can:

Notice what is missing from that list.

Your financing timeline.

Your runway.

Your need to close a round this quarter.

Strategic investors are not in business to solve your capital problem.

They are in business to solve their business problems.

Sometimes those interests align.

Often they don’t.

This is where founders get into trouble.

A large company agrees to meet.

Then another meeting.

Then a technical review.

Then a diligence session.

Then introductions to additional team members.

The founder becomes excited.

“We have strong strategic interest.”

Perhaps.

But strategic interest and investment intent are not the same thing.

I’ve seen companies spend six months, nine months, even a year pursuing a strategic relationship that ultimately resulted in nothing more than a better-informed strategic investor.

Not because anyone acted dishonestly.

Because learning was the objective.

Large organizations have an enormous capacity for curiosity.

They have a much smaller capacity for action.

For many strategic organizations, understanding a market, monitoring emerging technologies, evaluating competitive threats, and gathering intelligence are valuable outcomes by themselves.

A meeting is not a commitment.

Diligence is not a commitment.

Technical validation is not a commitment.

Even enthusiasm is not a commitment.

Founders who fail to recognize this often mistake activity for progress.

Another misconception is that strategic capital moves faster.

In reality, it is often the slowest money in the room.

Even when a strategic investor genuinely wants to invest, the process can involve:

A venture fund may make a decision in a week.

A strategic investor may need three months.

Or six.

Or longer.

This matters because fundraising is often a race against time.

Runway is finite.

Employees expect payroll.

Clinical milestones don’t wait.

Founders who build their financing strategy around a strategic investor often discover that the investor’s timeline and the company’s timeline have very little in common.

Here’s what many founders discover too late.

The best strategic investors often appear after a company becomes investable.

Not before.

This sounds backwards.

Most founders assume strategic investors help reduce risk.

In many cases, strategic investors show up after risk has already been reduced.

By the time a strategic investor becomes serious, the company often has:

Why?

Because strategic investors, like everyone else, prefer uncertainty to be lower rather than higher.

They are rarely rewarded internally for making speculative bets.

They are rewarded for making defensible decisions.

Proof points make those decisions easier.

Momentum makes those decisions easier.

An existing syndicate makes those decisions easier.

This leads to a surprising conclusion:

Many founders have the sequence backwards.

They assume strategic investors attract financial investors.

In reality, financial investors often attract strategic investors.

This is another lesson founders frequently miss.

A respected lead investor can do more to attract strategic interest than years of direct outreach.

Why?

Because strong financial investors perform a valuable function.

They validate.

They conduct diligence.

They provide credibility.

They reduce uncertainty.

When a reputable venture firm, family office, or institutional investor commits capital, strategic investors immediately gain confidence that someone else has already done substantial work.

That validation can become a powerful catalyst.

I’ve seen strategic interest increase dramatically after a financing closes.

Not before.

After.

Again, the sequence matters.

Before pursuing strategic investors, founders should ask themselves four questions.

Not pharma.

Not medtech.

Not healthcare.

This specific company.

What business objective are you helping them achieve?

Every strategic investment requires an internal champion.

Who benefits from your success?

Who is advocating for you internally?

FDA clearance?

Clinical data?

Commercial adoption?

Reimbursement?

Know what proof point they are waiting for.

This may be the most important question.

Many strategic relationships are worth pursuing for:

Not capital.

And that’s perfectly fine.

This lesson applies to investors as well.

Many investors become excited when a company claims it has strategic interest.

The next question should always be:

“What kind of strategic interest?”

A meeting is not validation.

A pilot is not validation.

An NDA is not validation.

An investment committee approval is validation.

A signed term sheet is validation.

The distinction matters.

Especially in life sciences.

Strategic investors can be extraordinary partners.

They can validate technologies.

Accelerate commercialization.

Open distribution channels.

Provide industry expertise.

And ultimately become acquirers.

But they are not superheroes.

They are not rescue capital.

And they are not in the business of solving a founder’s fundraising challenges.

The founders who navigate strategic relationships most effectively stop asking:

“How do we get a strategic investor?”

Instead, they ask:

“What would make us strategically relevant?”

The first question focuses on finding money.

The second focuses on creating value.

Over the long run, the companies that understand the difference tend to attract both.

© Big Idea CONNECTpreneur. All rights reserved. 2024